Return to Office Is Back. But This Is a Fundamentally Different Market.

The “return to office” narrative is often positioned as a recovery story, suggesting that the market is gradually returning to pre-2020 norms and behaviours.

In reality, what we are seeing is not a return, but a reset. There’s a shift into a more selective, more competitive market where occupiers are operating with greater scrutiny, more data, and a significantly higher expectation of what office space needs to deliver.

Supply Is quietly tightening, but with real impact

Recent reports suggest that in the UK’s regional office markets, the supply-demand balance is beginning to shift in a way that is not immediately visible, but is becoming increasingly important for occupiers making decisions today.

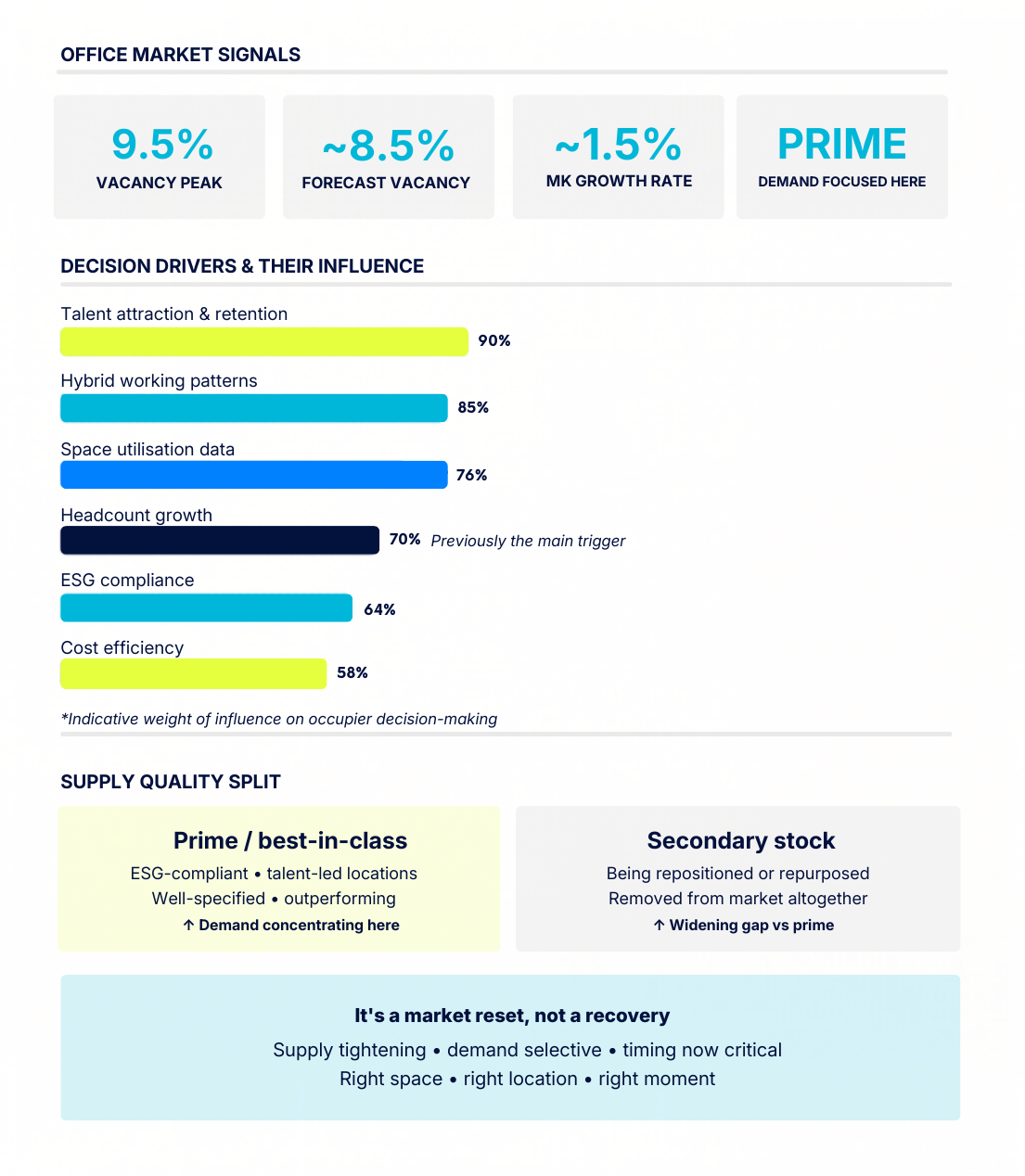

This tightening is not being driven by a surge in new demand, but by a sustained reduction in available space, with vacancy having already peaked at around 9-9.5% in recent years and now forecast to decline gradually towards ~8.5% over the medium term.

Together, these factors are contributing to a gradual reduction in vacancy across the market, with rates expected to fall from recent highs of around 9-9.5% towards the mid-8% range over the coming years.

For occupiers, this means that while choice still exists, the availability of high-quality, future-proofed space is becoming increasingly concentrated.

Decisions aren’t always driven by a single signal

Historically, office relocations or expansions were often triggered by a small number of clearly defined factors, with headcount growth being the most prominent and widely relied upon indicator.

While growth remains an important part of the picture, it is no longer sufficient on its own to explain how and when businesses make real estate decisions in today’s market.

Occupiers are now assessing a broader set of interdependent signals, often simultaneously:

Hybrid working patterns

Space utilisation

Cost efficiency

ESG performance

Talent attraction and retention

In this context, growth may initiate internal discussions, but it is the combination and alignment of these signals that ultimately drives action.

Demand is becoming increasingly concentrated around quality

The return to office is not being experienced evenly across the market, and instead is showing a clear pattern of concentration towards a specific type of product that meets modern occupational requirements.

Occupiers are not simply returning to office space, they are selectively choosing environments that support productivity, collaboration, and long-term business performance.

This is reflected in the continued outperformance of:

Prime, well-specified buildings

ESG-compliant space

Talent-led locations

At the same time, secondary stock is increasingly being repositioned, repurposed, or removed from the office market altogether, reinforcing the widening gap between best-in-class space and everything else.

This is no longer a short-term trend; it represents a structural reallocation of demand.

Occupiers are operating in a higher-stakes environment

With a more limited pool of high-quality options and a wider range of variables influencing decision-making, occupiers are under greater pressure to make the right move at the right time.

The decision-making process now requires a careful balance between competing priorities, where no single factor can be considered in isolation:

Flexibility vs commitment

Cost vs quality

Now vs future

In parallel, location strategy is becoming more closely linked to long-term competitiveness, particularly as access to talent, innovation clusters, and emerging technologies plays a greater role in business performance.

This is further reinforced by population trends, with key regional hubs such as Milton Keynes (~1.5%), Coventry (~1.4%) and Cambridge (~1.2%) significantly outperforming the UK average of ~0.8%.

Timing is becoming a defining factor in securing the right space

As supply tightens and demand becomes more focused, timing is emerging as a critical factor in the success of an occupier’s property strategy, particularly when the most competitive opportunities are no longer widely visible or openly marketed.

The best opportunities in the market are:

Secured earlier

Less publicly visible

Driven by insight, not reaction

For occupiers, this represents a clear shift in approach, where waiting for the “right opportunity” to appear is being replaced by the need to identify and act on the right signals ahead of the wider market.

It’s a market reset, not a recovery

The office market is not returning to a previous state, nor is it experiencing a broad-based rebound in demand, but instead is evolving into a more disciplined and data-driven environment where supply is constrained and demand is increasingly selective.

For occupiers, the opportunity lies not simply in taking space, but in securing the right space, in the right location, at the right moment - before those opportunities become increasingly limited.